Nonprofit Financial Hub

Bridge Loans for Nonprofits: Your Complete Guide to Filling Funding Gaps

Most nonprofits face these same challenge: funding doesn’t always arrive when you need it most. A major grant gets delayed. A capital campaign takes longer than expected. Or maybe a crucial donor payment gets pushed to next quarter. These timing mismatches can stall your mission right when momentum matters most.

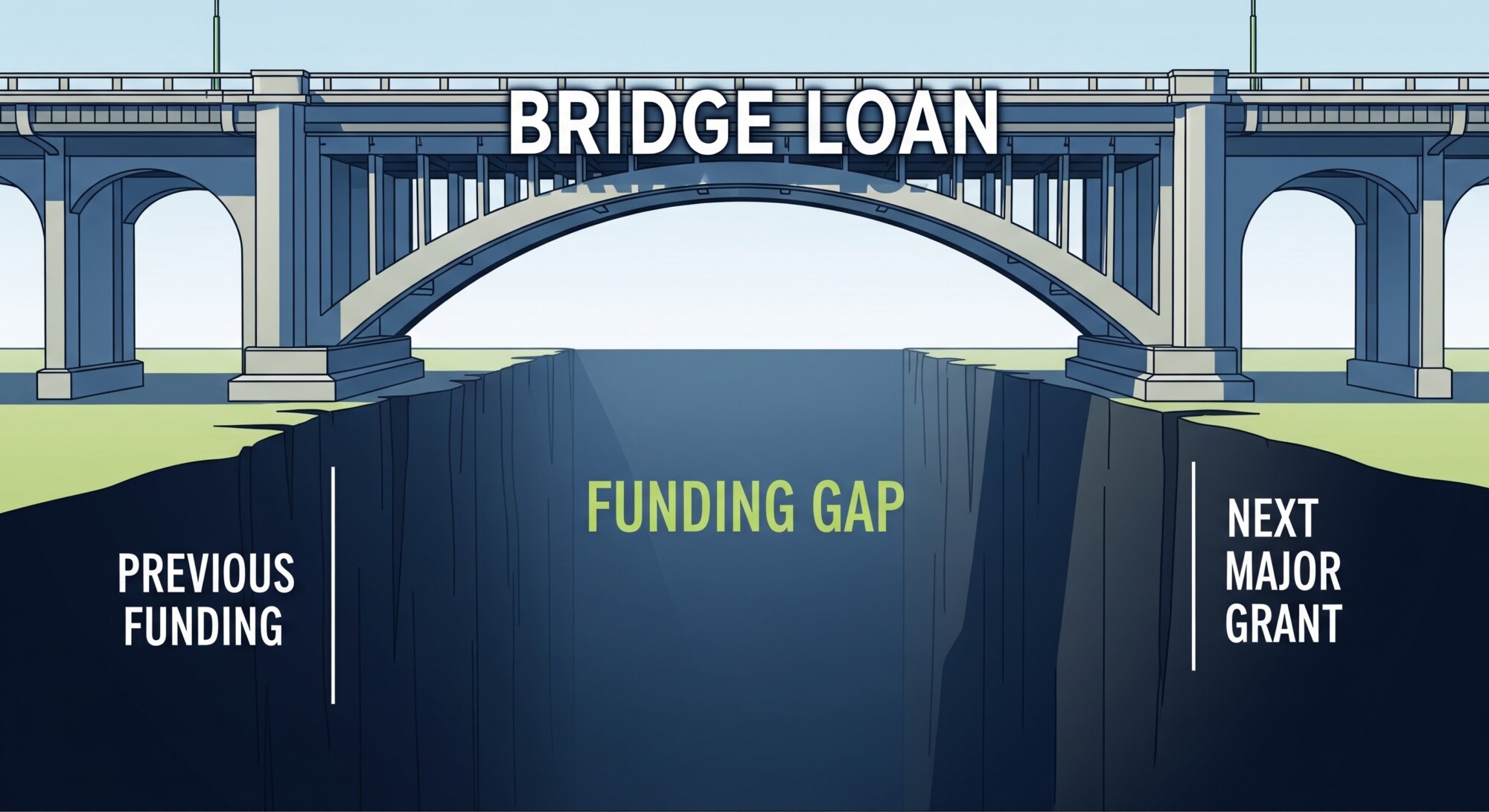

That’s where bridge loans come in. Think of them as financial bridges that help your organization cross from where you are today to where the money’s coming from tomorrow.

What Exactly Is a Nonprofit Bridge Loan?

A bridge loan is short-term financing designed to cover immediate expenses while you’re waiting for expected funds to arrive. It’s not about taking on debt you can’t repay, but rather accessing money you’ve already secured but just can’t touch yet.

For nonprofits, bridge loans typically range from $25,000 to several million dollars, with repayment terms anywhere from a few months to a couple of years. The key characteristic? You already know where the repayment money comes from.

Real-World Example: You’ve secured a $500,000 government grant for a new youth program, but the state won’t disburse funds for another six months. You need to hire staff and sign a lease now to launch on schedule. A bridge loan gives you the $500,000 today, and you repay it when the grant money arrives.

When Does a Bridge Loan Make Sense?

Bridge loans aren’t right for every situation, but they’re incredibly powerful in specific scenarios. Here’s when nonprofits typically turn to bridge financing:

- Delayed Grant Disbursements

Government grants and foundation awards often come with lengthy processing times. You’ve done the hard work of securing the grant, but bureaucratic delays mean you’re stuck waiting. A bridge loan lets you start the work immediately rather than putting your mission on hold.

- Capital Campaign Pledges

Your capital campaign was a success and you’ve raised $2 million in pledges for a new facility. But pledge payments are spread over three to five years, and construction costs are due now. Bridge financing allows you to break ground today and pay back the loan as pledge payments come in.

- Multi-Year Gift Commitments

A major donor commits to a $1 million gift paid out over four years. You could wait and slowly build your program, or you could use a bridge loan to launch at full scale immediately. Sometimes the right answer is to accelerate impact and pay down the loan with each annual installment.

- Reimbursable Grants

Many government contracts and grants work on a reimbursement basis where you need to spend the money first and get paid back later. For smaller nonprofits without deep cash reserves, this creates a serious problem. Bridge loans provide the upfront capital to fulfill the contract requirements.

- Lost or Delayed Major Gifts

Let’s say a major donor pledges $300,000 but then faces unexpected personal financial challenges and asks to delay payment by a year. You’ve already budgeted that revenue and made commitments based on it. Rather than cutting programs or laying off staff, a bridge loan maintains continuity until that gift comes through.

Facing a Funding Gap?

B Generous specializes in bridge loans and flexible financing solutions designed specifically for nonprofits. Our application process takes less than 30 minutes, with preliminary decisions on completed applications usually provided in 10-14 business days.

How Bridge Loans Differ from Traditional Loans

While bridge loans are a type of loan, they work quite differently from standard term loans or lines of credit:

| Feature | Bridge Loan | Traditional Term Loan |

|---|---|---|

| Duration | 3-24 months | 2-5+ years |

| Purpose | Cover gap until specific funds arrive | General operating expenses or capital projects |

| Repayment Source | Known, identified funding | General organizational revenue |

| Speed | Fast approval (1-2 weeks) | Longer process (4-10 weeks) |

| Best For | Timing mismatches | Long-term investments |

What Lenders Look for When Approving Bridge Loans

Bridge loan approval focuses on one critical question: How confident can we be that the expected funds will actually arrive? Here’s what lenders typically evaluate:

Documentation of Expected Funds

You’ll need concrete proof that money is coming. This might include:

- Signed grant award letters from government agencies or foundations

- Written pledge commitments from major donors

- Multi-year gift agreements with payment schedules

- Government contracts showing reimbursement terms

- Capital campaign documentation with pledge cards

Organizational Financial Health

Organizational Financial Health

Even with documented future funds, lenders want to see that your organization is fundamentally stable. They’ll review:

- Recent financial statements (typically the current year and 2 prior yeasr)

- Your Form 990 submissions

- Current operating budget

- Cash flow projections

- Any existing debt obligations

Organizational Track Record

Lenders feel more comfortable with nonprofits that have a proven history. Factors that strengthen your application:

- Years in operation (3+ years is ideal)

- History of successfully managing previous grants or large gifts

- Strong board governance and oversight

- Demonstrated financial management capability

Good to Know: Some lenders, including B Generous, specialize in working with younger nonprofits or organizations with limited collateral. Don’t assume you won’t qualify. It’s often worth exploring your options.

The Bridge Loan Application Process

Applying for a nonprofit bridge loan is typically more straightforward than you might expect. Here’s what the process usually looks like:

Step 1: Simple Online Pre Qualification

Most lenders, including B Generous, begin the application process with a straightforward online pre-qualification form to ensure that both your nonprofit and the lender are an appropriate fit.

Step 2: Documentation Submission

You’ll compile and submit the necessary paperwork. At a minimum, expect to provide:

- Completed loan application

- Recent financial statements and Form 990s

- Documentation of expected funds (grant letters, pledges, etc.)

- Organizational documents (bylaws, board roster, 501(c)(3) determination letter)

- Brief narrative about your mission and the need for bridge financing

Step 3: Credit Review

The lender’s credit team reviews your application and supporting documents. They’re assessing both the certainty of the expected funds and your organization’s overall financial health. This typically takes one to two weeks.

Step 4: Loan Terms and Approval

If approved, you’ll receive a term sheet outlining the loan amount, interest rate, repayment schedule, and any other conditions. Review this carefully. You’re not obliged to accept this until you sign the final loan documents.

Step 5: Closing and Funding

Once you accept the terms and complete final paperwork, funds are typically disbursed within a few days. The entire process from initial application to funded loan usually takes under 30 days from the completed application for most bridge loan scenarios.

Understanding Bridge Loan Costs

Bridge loans typically cost more than traditional long-term financing, but that’s because you’re paying for speed, flexibility, and convenience. Here’s what to expect:

Interest Rates

Nonprofit bridge loan rates typically range from high single digits to the low-to-mid teens depending on:

- The strength of your repayment source

- Your organization’s financial position

- Current market interest rates

- The loan duration

Fees

Some bridge loans include upfront fees, while others don’t. When comparing options, look at:

- Application fees (many lenders charge nothing)

- Origination fees (typically 0-2% of loan amount)

- Prepayment penalties (some lenders charge if you pay off early, others don’t)

At B Generous, for example, there are no upfront costs or application fees and you only pay us if you accept and close on a loan offer.

Is the Cost Worth It?

Here’s a helpful way to think about bridge loan costs: compare what you’ll pay against what you’ll gain. If a $200,000 bridge loan costs $10,000 in interest but allows you to:

- Start a program six months earlier, serving 100 additional families

- Avoid laying off three staff members

- Secure a facility before it goes to another buyer

- Take advantage of a matching gift opportunity

…then the value often far exceeds the cost. It’s about mission impact, not just financial calculations.

Need Expert Guidance?

Our team helps nonprofits evaluate whether bridge financing makes sense for their specific situation. Connect with us for a no-obligation consultation.

Alternatives to Bridge Loans

Bridge loans are powerful, but they’re not the only option. Depending on your situation, you might also consider:

Lines of Credit

A line of credit for nonprofits works like a credit card. You can draw funds as needed and only pay interest on what you use. If you face frequent but unpredictable cash flow gaps, a line of credit might provide more flexibility than individual bridge loans.

Working with Your Donor or Grantor

Sometimes the simplest solution is asking if payments can be accelerated. A foundation might be willing to move up a grant disbursement date. A major donor might be able to make a gift earlier than originally planned. It never hurts to ask.

Temporarily Redirecting Unrestricted Funds

If you have unrestricted reserves, you might use those to cover the gap and replenish them when the expected funds arrive. This only works if you have sufficient reserves and won’t jeopardize operations by temporarily reducing them.

Campaign Against the Pledge

Some larger nonprofits can get funding from banks using their pledge commitments as collateral. This typically requires substantial pledges from creditworthy donors and might involve personal guarantees from board members.

Common Bridge Loan Mistakes to Avoid

Bridge loans are straightforward, but organizations sometimes stumble. Here are pitfalls to watch for:

Overestimating Funding Certainty

Be honest about how certain your expected funds really are. A verbal commitment from a donor isn’t the same as a signed pledge. A grant you’ve applied for but haven’t been awarded yet shouldn’t be treated as secured funding. Only bridge against money you can document with certainty.

Ignoring the Timeline

Make sure your bridge loan term extends beyond when you expect funds to arrive. If a grant is “supposed” to come in six months, consider a 12-month bridge loan term to give yourself cushion. Delays happen, and you don’t want to be scrambling to refinance if the timeline stretches.

Failing to Have a Plan B

What if the expected funds fall through entirely? Before taking a bridge loan, make sure you have a contingency plan for repayment even if the primary source doesn’t materialize. This might mean having unrestricted reserves you could tap, or other fundraising plans you could accelerate.

Not Reading the Fine Print

Understand all loan terms before signing. Are there prepayment penalties? What happens if you need to extend the loan term? Are there any financial covenants you need to maintain? Don’t be afraid to ask questions—any reputable lender will be happy to explain.

Success Stories: Bridge Loans in Action

Real examples help illustrate how bridge financing creates impact:

Educational Nonprofit in Florida

“We faced a massive funding delay from the state. B Generous stepped in when we had no other options. Their financing truly saved our organization.”

This organization used a bridge loan to maintain operations during a state-wide delay in education funding disbursements. Without the bridge loan, they would have had to lay off teachers and cut programs mid-school-year.

Youth Homelessness Organization

“As a young nonprofit with limited collateral, we didn’t think financing was possible. B Generous proved us wrong and helped us secure the funding we needed to grow. They really were a godsend.”

This newer organization secured a significant foundation grant but needed upfront capital to lease a facility and hire staff before grant funds were disbursed. A bridge loan made it possible to launch their program on schedule.

Women’s Health Nonprofit

“Waiting on grant disbursements used to stall our programs. Now, with B Generous, we have breathing room—and can generate impact on our own terms.”

After experiencing how bridge financing solved one crisis, this organization now proactively uses bridge loans as a strategic tool, allowing them to move quickly on opportunities without waiting for grant payment timing.

Is Your Nonprofit Ready for a Bridge Loan?

Ask yourself these questions to determine if bridge financing makes sense right now:

Do we have documented, committed funding that just hasn’t been received yet?

Is waiting for those funds causing us to miss critical opportunities or risk mission impact?

Do we have a clear timeline for when the expected funds will arrive?

Can we demonstrate financial stability and responsible financial management?

Do we have a backup plan if the expected funds are delayed?

Have we calculated that the cost of the bridge loan is worthwhile compared to waiting?

If you answered “yes” to most of these questions, a bridge loan might be exactly what your organization needs.

Next Steps: Getting Your Bridge Loan

Ready to explore bridge financing for your nonprofit? Here’s how to move forward:

- Gather Your Documentation: Compile your financial statements, grant letters, pledge commitments, and organizational documents. Having these ready will speed up the process.

- Connect with a Nonprofit Lender: Reach out to lenders who specialize in nonprofit financing. They understand your unique needs and can move quickly.

- Have an Honest Conversation: Be transparent about your situation, your timeline, and your repayment source. The more candid you are, the better the lender can structure a solution that works.

- Review Options Carefully: Don’t feel pressured to accept the first offer. Compare terms, ask questions, and make sure you understand exactly what you’re signing up for.

- Plan for Success: Once funded, use the bridge loan strategically to maximize mission impact. And document the results—future funders will be impressed by how thoughtfully you managed this financing tool.

Get Started with B Generous

B Generous is America’s leading nonprofit lending marketplace, trusted by thousands of nonprofits nationwide. We’ve approved nearly $100 million in loans to organizations just like yours, helping them navigate funding gaps and accelerate their missions.

Our application takes less than 30 minutes to complete, and most organizations receive a preliminary credit decision within one to two weeks after we receive a completed application. There are no application fees, no upfront costs, and Most financing options through B Generous do not require personal guarantees.

Whether you need a bridge loan, a line of credit, or another financing solution, our team is here to help you find the right answer for your nonprofit’s unique needs

Explore nonprofit financing solutions or Apply Now

About B Generous

B Generous empowers nonprofits and charitable organizations with fast, flexible access to the capital they need to focus on what matters most, advancing their mission. Through our industry-leading nonprofit lending marketplace, organizations can secure funding quickly and efficiently, from $25,000 to $50 million.

Disclaimer:

All examples, case studies, timelines, and cost calculations in this article are illustrative only and are not guarantees of terms, pricing, approval, or funding speed. Actual financing structures, interest rates, fees, and timelines depend on the borrower’s financial condition, documentation, collateral, and other underwriting factors. This content is provided for educational purposes and does not constitute financial, legal, or investment advice.